Answers to Important Illinois Tax Questions

On January 18, our Illinois Tax Issues & Updates webinar was packed full with nearly 1,000 attendees. The audience was very engaged, and over 100 questions came in during the…

As the 2023 filing season begins, taxpayers and their preparers must sort through new guidance and rules to determine their requirements for the 2022 tax year. This post details 10 key considerations for these returns.

On January 12, the IRS announced that it would begin accepting individual tax returns on January 23, 2023. Most individual tax returns are due April 18, 2023, because April 15 falls on a Saturday and Emancipation Day falls on Monday, April 17. The IRS began accepting business returns on January 12, 2023. Fourth quarter estimates (and single estimated tax payments for qualified farmers) were due January 17, 2023.

The child tax credit for 2022 is $2,000 per child, available only for qualifying children under the age of 17. The credit is partially refundable in 2022 in an amount up to 15% of the taxpayer’s earned income in excess of $2,500, or, if more, for taxpayers with three or more qualifying children, to the extent the taxpayer’s social security taxes exceed the taxpayer’s earned income credit. The refundable credit cannot exceed $1,500 for any child for 2022. The child tax credit begins to phase-out in 2022 when modified adjusted gross income exceeds $200,000 for single filers and $400,000 for those married filing jointly. The phase-out also applies to the $500 other dependent credit available for dependents over the age of 16.

These are big changes from last year’s child tax credit. In 2021, the credit was temporarily increased to $3,000 for children ages six through 17 (17 year olds were included) and $3,600 for children under six. Significantly, the entire credit was refundable, meaning that it was available to those with no earned income.

For 2022, taxpayers can take a maximum $1,050 child and dependent care credit for one qualifying individual and a maximum of a $2,100 credit for more than one qualifying individual. The credit is not refundable. This credit is based upon 20% to 35% of eligible expenses (up to $3,000 for one qualifying individual and $6,000 for more than one qualifying individual) paid to care for the qualifying individual so that the taxpayer can work. The percentage of expenses used to calculate the credit is based upon AGI.

In 2021, the American Rescue Plan Act had temporarily and significantly increased this credit. Taxpayers were eligible for a credit in an amount up to $4,000 for one qualifying individual and $8,000 for more than one qualifying individual. The credit was refundable for most taxpayers.

In 2022, only taxpayers who itemize deductions may take a charitable contribution deduction. The above-the-line charitable contribution deduction available in 2020 and 2021 was not extended. Additionally, for 2022, the contribution base for individuals has returned to 60 percent for cash contributions and 30 percent for noncash contributions

In 2020, taxpayers who did not itemize deductions could take an above-the-line charitable contribution deduction up to $300 per return. In 2021, this maximum deduction was increased to $600 for those married filing jointly.

In 2022, the U.S. Department of Education initiated a Student Debt Relief Plan seeking to cancel $10,000 of student loan debt for millions of eligible students and $20,000 for eligible Pell grant recipients. If this program is implemented, the forgiven debt would not be taxable because the American Rescue Plan Act excludes canceled student loan debt from taxation. The future of this plan is uncertain, however, as opponents have filed court challenges alleging that the administration was seeking to unconstitutionally exercise Congressional power. The U.S. Supreme Court has agreed to hear this challenge on February 28, 2023.

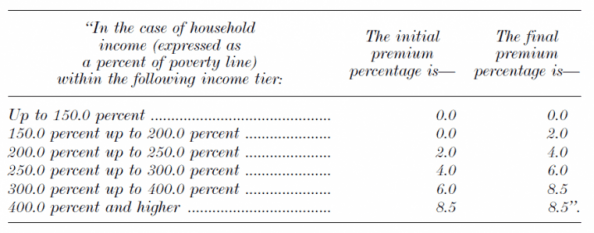

In 2022, taxpayers are eligible for an enhanced premium tax credit made available by the American Rescue Plan Act. This provision was first implemented in 2021, and will remain in effect through 2025 because of an extension in the Inflation Reduction Act.

Under these provisions, taxpayers with household income above 400 percent of the federal poverty line will continue to qualify for premium tax credits if the second lowest silver plan would cost them more than 8.5 percent of household income. The Act also lowers the applicable percentages of household income (which determines the amount of the required premium) for all income levels. The following table depicts the final premium percentages through 2025. Taxpayers must only pay premiums in an amount up to the final premium percentage of household income. The premium tax credit pays the difference.

Beginning in 2023, final administrative rules eliminating the so-called “family glitch” are also in effect. The administration issued these rules, TD 9968, in October 2022. They provide that the affordability of employer coverage for family members of an employee is determined based on the employee’s share of the cost of covering the employee and those family members, not the cost of covering only the employee. This means that premium tax credits may be available to those for whom individual, but not family, coverage is affordable. Under these provisions, a plan is not affordable if the employee’s contribution for the family coverage is more than 9.5 percent of the applicable household income.

In 2022, taxpayers may take a 100 percent deduction for qualifying business meals where the food or beverages were provided by a restaurant. Other business meals are allowed a 50 percent deduction. Notice 2021-63 allows taxpayers to treat the entire meal portion of the per diem rate as being attributable to food provided by a restaurant.

In 2023, there is no enhanced deduction for business meals from a restaurant. This special provision was in place only for tax years 2021 and 2022.In 2023, taxpayers may deduct 50 percent of the cost of otherwise-eligible business meals.

Two standard mileage rates apply to tax year 2022. The rate was adjusted July 1, 2022, because of increased fuel costs. The deduction for miles driven from January 1 through June 30, 2022, is 58.5 cents per mile for business miles and 18 cents per mile for medical and moving miles. The rate is increased for miles driven from July 1, 2022, through December 31, 2022, to 62.5 cents per mile for business miles and 22 cents per mile for medical and moving miles. The rate for charitable miles remains at 14 cents per mile for all periods.

In 2023, the rate for business miles increases to 65.5 cents per mile and remains at 22 cents per mile for medical and moving miles and 14 cents per mile for charitable miles.

The American Rescue Plan Act provided that, for tax year 2022, third party networks would be required to provide 1099-K’s if aggregate transactions exceeded $600. Prior to 2022, Form 1099-K was issued for third party payment network transactions only if the total number of transactions exceeded 200 for the year and the aggregate amount of these transactions exceeded $20,000.

In Notice 2023-10, IRS delayed these reporting requirements for the 2022 tax reporting year: With respect to returns for calendar years beginning before January 1, 2023, a third party settlement organization is not required to report payments in settlement of third party network transactions with respect to a participating payee unless the gross amount of aggregate payments to be reported exceeds $20,000 and the number of such transactions with that participating payee exceeds 200.

In 2021, IRS began requiring pass through entities with items of international tax relevance to file Schedules K-2 and K-3 with the IRS and provide Schedules K-3 to partners and shareholders. The IRS stated that the new forms were required to help partners and partnerships and shareholders and S corporations comply with international tax rules implemented with the Tax Cuts and Jobs Act of 2017.

Because the new reporting requirements caused confusion, IRS provided transitional relief in 2021. Entities were required to exercise “good faith” in providing necessary information for the 2021 tax year. If a domestic partnership or S corporation had no knowledge that the partners or shareholders were requesting the K-3 information for tax year 2021, they were not required to prepare the K-2 or the K-3.

For 2022, IRS has issued new guidance through final Partnership Instructions for Schedules K-2 and K-3 (dated December 23, 2022). The final instructions provide a “domestic filing exception,” which has refined earlier guidance provided in October draft instructions. IRS has provided a similar instruction for S Corporations. Specifically, the latest instructions eliminate a need for partnerships and S corporations to provide advance notice to partners and shareholders. Rather, the notice requirement is satisfied with an attachment to a timely filed K-1.

The partnership instructions, for example, provide that the partnership does not need to (a) complete and file with the IRS the Schedules K-2 and K-3, or (b) furnish to a partner the Schedule K-3 (except where requested by a partner after the 1-month date (defined in criteria number 4, below)) if each of the following four criteria are met with respect to the partnership’s tax year 2022:

1. The partnership has no or “limited” foreign activity.

2. The partnership has all U.S. citizen/resident alien partners.

3. The partnership follows the notification requirements.

4. No 2022 Schedule K-3 is requested by the 1-month date.

Original article published January 16, 2023. Reprinted here with permission.

By Kristine Tidgren

Director, Center for Agricultural Law & Taxation

Adjunct Assistant Professor, Agricultural Education

Iowa State University

Disclaimer: The information referenced in Tax School’s blog is accurate at the date of publication. You may contact taxschool@illinois.edu if you have more up-to-date, supported information and we will create an addendum.

University of Illinois Tax School is not responsible for any errors or omissions, or for the results obtained from the use of this information. All information in this site is provided “as is”, with no guarantee of completeness, accuracy, timeliness or of the results obtained from the use of this information. This blog and the information contained herein does not constitute tax client advice.

Join 1,400 of your colleagues and get notified each time a new post is added.